Jim Teague's planned retirement as co-CEO of Enterprise Products Partners after 28 years represents a significant leadership transition at a company that functions as critical infrastructure for US petrochemical manufacturing. Enterprise Products operates the pipeline networks, fractionation facilities and storage terminals that enable natural gas liquids and petrochemical feedstocks to flow from production regions to chemical plants throughout Texas, Louisiana and the broader Gulf Coast industrial corridor. For procurement teams managing ethylene, propylene, butadiene and derivative chemical sourcing, changes at companies controlling these logistics arteries warrant attention because infrastructure reliability and access terms directly affect material availability and delivered costs.

Randall Fowler will continue as sole chief executive following Teague's departure, ending the co-CEO structure that characterized Enterprise Products' governance for several years. The transition occurs as the company manages over 50,000 miles of pipelines, 260 million barrels of storage capacity and processing assets that handle millions of barrels daily of the NGLs that serve as primary feedstocks for the petrochemical industry.

The Infrastructure Chemical Buyers Actually Depend On

Enterprise Products' asset footprint touches nearly every major petrochemical production hub in North America. The company's NGL pipelines connect Permian Basin, Eagle Ford and other production regions to fractionation plants along the Gulf Coast where mixed NGL streams get separated into specification-grade ethane, propane, normal butane, isobutane and natural gasoline.

These fractionated products feed directly into chemical manufacturing. Ethane serves as the primary feedstock for ethylene production through steam cracking. Propane can be dehydrogenated to produce propylene for polypropylene, acrylonitrile and other derivatives. Butanes feed into alkylation units and serve as feedstocks for butadiene and synthetic rubber production.

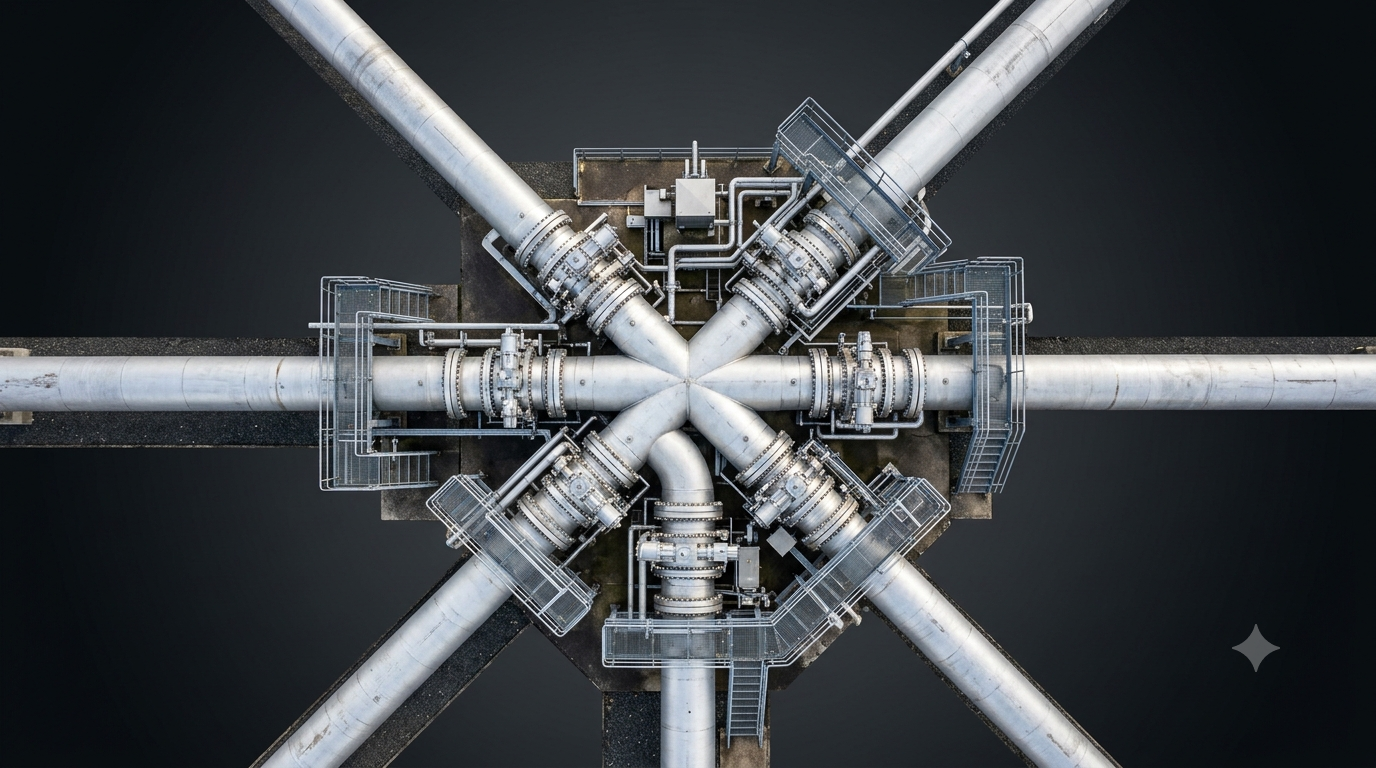

Enterprise Products also operates dedicated petrochemical pipelines including the ATEX pipeline system delivering ethylene from Mont Belvieu to consuming plants across Texas and the propylene pipeline network serving similar distribution functions. These pipelines enable just-in-time delivery of feedstocks to chemical plants without requiring on-site storage for weeks of inventory.

The storage capacity Enterprise Products controls at Mont Belvieu and other hubs provides the buffer capacity that smooths supply-demand imbalances and enables trading activities that establish benchmark pricing for NGLs and petrochemicals. Disruptions to this storage infrastructure or changes in access terms would ripple through chemical supply chains extending far beyond companies that directly contract with Enterprise Products.

NGL Fractionation Bottlenecks and Capacity Access

Fractionation capacity represents a potential bottleneck in NGL-to-petrochemical supply chains. Raw NGLs produced at gas processing plants must be separated into individual components before they can be used as chemical feedstocks. Insufficient fractionation capacity creates situations where mixed NGLs back up in pipelines, forcing production curtailments or suboptimal blending.

Enterprise Products operates multiple large-scale fractionation trains at Mont Belvieu with total capacity exceeding 1 million barrels per day. The company has historically invested in capacity expansions ahead of demand growth, maintaining the processing capability needed to handle increasing NGL production from shale basins.

Leadership transitions sometimes trigger reassessments of capital allocation priorities. A new sole CEO might evaluate whether continued fractionation expansion serves shareholder interests or whether capital should shift toward higher-return opportunities in other business segments. Chemical buyers should monitor whether Enterprise Products maintains its historical pattern of proactive capacity investment or adopts a more conservative approach.

Fractionation capacity constraints affect chemical manufacturers indirectly through feedstock availability and pricing. When fractionation capacity is tight, ethane and propane prices can disconnect from their typical relationships to crude oil and natural gas because physical logistics constraints override normal supply-demand fundamentals.

Geographic Concentration Risk in Gulf Coast Infrastructure

The US petrochemical industry's concentration along the Gulf Coast creates both efficiencies and vulnerabilities. Enterprise Products' infrastructure serves this concentrated geography with extensive pipeline networks, storage terminals and processing facilities optimized for the region's production and consumption patterns.

This concentration means that disruptions affecting Enterprise Products assets can impact a large share of US petrochemical production simultaneously. Hurricane events, industrial accidents, cybersecurity incidents or operational issues that take infrastructure offline affect multiple chemical producers relying on the same logistics systems.

The 2021 Winter Storm Uri demonstrated how infrastructure vulnerabilities propagate through chemical supply chains. Freeze-offs at processing facilities, power outages affecting pumping stations and pipeline restrictions created cascading disruptions that shut down chemical plants throughout Texas and Louisiana for days or weeks.

Enterprise Products' infrastructure performed relatively well during that event compared to some competitors, but the episode illustrated how chemical manufacturing depends on continuous infrastructure operation. Leadership changes that might affect maintenance practices, investment priorities or operational philosophies could influence infrastructure reliability over time.

How Tariff Structures Affect Chemical Economics

Midstream companies earn revenue primarily through tariffs charged for pipeline transportation, processing fees for fractionation and storage fees for tankage. These tariffs directly affect the delivered cost of feedstocks to chemical manufacturers and therefore influence chemical production economics and competitive positioning.

Enterprise Products operates assets under various tariff structures including FERC-regulated pipelines with published rates, negotiated rate agreements with specific shippers and market-based services without regulatory rate controls. The mix of regulatory frameworks creates complex pricing that chemical buyers must navigate when evaluating feedstock sourcing options.

Leadership transitions can influence commercial strategies around tariff setting, contract renewal negotiations and willingness to offer volume discounts or long-term rate commitments. A CEO focused on maximizing near-term cash flow might pursue aggressive rate increases, while one prioritizing long-term customer relationships might maintain stable, predictable pricing.

Chemical companies with significant volume moving through Enterprise Products infrastructure should view the leadership transition as an opportunity to assess relationship health, evaluate contract terms approaching renewal and ensure that commercial relationships receive appropriate senior-level attention during the transition period.

Ethylene Pipeline Networks and Just-in-Time Manufacturing

The petrochemical industry increasingly operates on just-in-time principles where chemical plants maintain minimal feedstock inventory and depend on continuous pipeline delivery. Enterprise Products' ethylene pipeline network enables this operating model by providing reliable, high-volume transportation from cracker facilities to derivative plants producing polyethylene, ethylene oxide, styrene and other products.

Disruptions to ethylene pipeline service force derivative plants to curtail production within hours as on-site storage depletes. Unlike crude oil or finished products that can be transported via truck or rail as backup options, ethylene requires pipeline or specialized cryogenic tankers due to its gaseous state and handling requirements.

This dependency on continuous pipeline service means that chemical plant operators need confidence in infrastructure reliability and operator competence. A leadership transition at the company controlling critical ethylene infrastructure introduces questions about whether operational excellence and reliability culture will be maintained under new leadership.

Enterprise Products has maintained strong operational performance across its asset base for decades. The company's safety record, uptime statistics and incident frequency compare favorably to industry peers. Maintaining this performance through leadership transitions requires effective knowledge transfer and cultural continuity that cannot be taken for granted.

Storage Capacity and Market Making Functions

Enterprise Products' storage capacity at Mont Belvieu and other locations serves functions beyond simple inventory holding. These storage facilities enable trading activities, provide flexibility for producers and consumers managing supply-demand imbalances and help establish the price discovery mechanisms that set benchmark values for NGLs and petrochemicals.

Chemical buyers benefit from liquid, transparent markets where prices reflect supply-demand fundamentals rather than logistical artifacts or information asymmetries. Storage infrastructure operated by neutral parties like Enterprise Products supports this market function by enabling multiple producers and consumers to access common storage pools.

Changes in storage access policies, fee structures or operational practices could affect market liquidity and price transparency in ways that disadvantage some market participants while benefiting others. Chemical procurement teams should monitor whether the leadership transition brings changes to storage operations or commercial policies that might affect their ability to manage feedstock price risk or secure favorable delivery terms.

The financial derivatives markets for NGLs and petrochemicals depend on physical storage capacity and the arbitrage activities that keep futures prices aligned with spot market realities. Enterprise Products' storage assets play important roles in these market mechanisms, making the company's operational and commercial decisions relevant even to buyers who never directly contract for storage services.

Alternative Infrastructure and Competitive Dynamics

Enterprise Products faces competition from other midstream companies including Energy Transfer, MPLX, Targa Resources and DCP Midstream that operate overlapping infrastructure serving similar geographic areas and customer bases. This competitive landscape provides options for chemical manufacturers evaluating feedstock logistics strategies.

However, the capital intensity and long construction timelines for pipelines, fractionators and storage terminals mean that competitive alternatives cannot quickly materialize to address service issues or unfavorable commercial terms at incumbent providers. A chemical plant connected exclusively to Enterprise Products infrastructure may face multi-year timelines and eight-figure capital costs to establish alternative pipeline connections.

This creates path dependencies where historical infrastructure decisions constrain current options. Chemical companies planning new facilities or expansions should evaluate whether to design for single-infrastructure-provider dependency or invest in redundant connections that preserve competitive options and operational flexibility.

The leadership transition at Enterprise Products provides a useful reminder that infrastructure providers are businesses with evolving strategies rather than static utilities. Procurement and operations teams should periodically reassess infrastructure dependencies and evaluate whether investments in alternative connections or backup logistics capabilities justify their costs.

What the Track Record Shows

Teague's 28-year tenure provides extensive track record for evaluating Enterprise Products' historical approach to customer relationships, infrastructure investment and operational reliability. The company consistently invested in capacity expansions ahead of demand growth, maintained conservative financial leverage and prioritized operational uptime over cost minimization.

This track record created a reputation for reliability that chemical manufacturers value highly. The question going forward is whether Fowler as sole CEO will maintain these priorities or adjust the company's balance between growth investment, financial returns to unitholders and service quality.

Fowler's background includes decades with Enterprise Products in senior operating and commercial roles, suggesting continuity is more likely than dramatic strategic shifts. However, removing the co-CEO structure concentrates decision-making authority and eliminates the checks and balances that dual leadership provides.

Chemical buyers should monitor several indicators over the next 12 to 24 months including capital spending announcements relative to historical patterns, service quality metrics like pipeline availability and on-time delivery performance and commercial terms offered in contract renewals or new customer negotiations.

Integration with Broader Logistics Networks

Enterprise Products infrastructure does not operate in isolation but connects to broader logistics networks including marine terminals for NGL and petrochemical exports, rail loading facilities and connections to other pipeline systems serving different geographic regions. The company's commercial strategies around these integration points affect chemical buyers' options for sourcing feedstocks from alternative regions or accessing export markets for finished products.

The US has become a major exporter of petrochemicals and derivatives as domestic production capacity has grown faster than consumption. Enterprise Products operates export terminals that handle ethane, propane, ethylene and other materials serving international markets. The balance between domestic and export flows affects US domestic pricing and availability.

Leadership decisions about export infrastructure investment and access policies influence whether domestic chemical manufacturers face increasing competition from exports for feedstock supplies. Chemical buyers should track whether Enterprise Products continues expanding export capabilities or shifts focus toward serving domestic markets.

Financial Strength and Operational Sustainability

Enterprise Products' financial position affects its ability to maintain and expand infrastructure that chemical supply chains depend on. The company operates as a master limited partnership (MLP) with distribution requirements to unitholders that consume significant cash flow. This structure has historically worked well but creates financial obligations that might constrain discretionary investment during industry downturns.

The leadership transition does not change Enterprise Products' financial structure, but a new CEO's approach to balancing distributions versus retained capital for growth could shift. Chemical buyers reliant on the company's infrastructure have interest in Enterprise Products maintaining financial strength sufficient to fund ongoing maintenance, regulatory compliance and capacity expansions that prevent bottlenecks.

Companies whose supply chains depend heavily on single infrastructure providers should monitor those providers' financial health, credit ratings and distribution coverage ratios. Early warning signs of financial stress provide time to develop contingency plans before service disruptions materialize.

Regulatory Environment and Infrastructure Expansion

New pipeline construction and capacity expansions face increasingly complex permitting processes involving federal, state and local regulatory approvals plus stakeholder opposition in many regions. These challenges extend project timelines and increase costs in ways that can make infrastructure investments economically unattractive despite underlying demand.

Enterprise Products' ability to continue expanding infrastructure capacity depends partly on navigating these regulatory environments successfully. Leadership with strong government relations capabilities and track records of obtaining permits matters for companies whose business models require ongoing infrastructure buildout.

The retirement of a 28-year veteran removes institutional knowledge about regulatory relationships and permitting strategies that cannot be fully transferred through transition planning. Chemical buyers should assess whether Enterprise Products maintains permitting momentum on projects important to feedstock access or whether regulatory challenges increase under new leadership.

Positioning for the Energy Transition

Midstream companies including Enterprise Products face strategic questions about their roles in energy transition scenarios where fossil fuel demand potentially declines over multi-decade timeframes. Different leadership teams might take dramatically different approaches to balancing traditional hydrocarbon infrastructure with investments in hydrogen pipelines, CO2 transport for carbon capture or renewable fuels logistics.

These strategic choices affect long-term infrastructure availability for petrochemical feedstocks. A midstream company that aggressively pivots toward alternative energy infrastructure might underinvest in NGL and petrochemical logistics even if near-term demand remains strong.

Chemical manufacturers planning production footprints for the 2030s and beyond need visibility into infrastructure providers' long-term strategies. The leadership transition provides opportunity for Enterprise Products to articulate its energy transition positioning and for customers to assess whether that positioning aligns with their own planning assumptions.

What Procurement Teams Should Do Now

Chemical procurement teams whose supply chains involve Enterprise Products infrastructure should take several near-term actions. First, review existing transportation, fractionation and storage contracts to understand expiration dates, renewal terms and whether contracts provide adequate volume commitments and pricing predictability.

Second, establish or refresh relationships with Enterprise Products commercial teams under the new leadership structure. Ensure that your company is viewed as a valued customer and that communication channels function effectively for addressing service issues or discussing capacity needs.

Third, evaluate whether your infrastructure dependency on Enterprise Products creates unacceptable concentration risk. Model scenarios where service disruptions, unfavorable contract renewals or capacity constraints force alternative logistics solutions and assess whether investments in redundant infrastructure connections are justified.

Fourth, monitor Enterprise Products' capital spending announcements, project approvals and commercial partnerships for signals about strategic priorities under sole-CEO leadership. Significant changes in investment patterns or market focus could affect feedstock availability and pricing in regions or product categories important to your supply chain.

Fifth, benchmark Enterprise Products' service quality, commercial terms and infrastructure availability against alternative providers to ensure you maintain realistic understanding of competitive options should relationships or service levels deteriorate.

The leadership transition at Enterprise Products represents a natural evolution for a company built over decades by a small group of executives. Continuity appears more likely than disruption given Fowler's long tenure and the company's established strategic direction. However, chemical buyers whose manufacturing operations depend on continuous, reliable access to NGL and petrochemical logistics infrastructure should treat this transition as a prompt to reassess dependencies, refresh relationships and ensure that contingency plans exist for scenarios where preferred infrastructure access becomes constrained or uneconomical.

Ready to source Styrene Monomer from verified global suppliers? Explore competitive offers on our platform today.