Article

Jun 12, 2026schedule5 Min Read

India's Chemical Industry in a Pivotal June: Duty Waiver End

June 2026 is the most consequential month for India's chemical industry in years.

Full Reportarrow_forward

prodchem

Jun 12, 2026

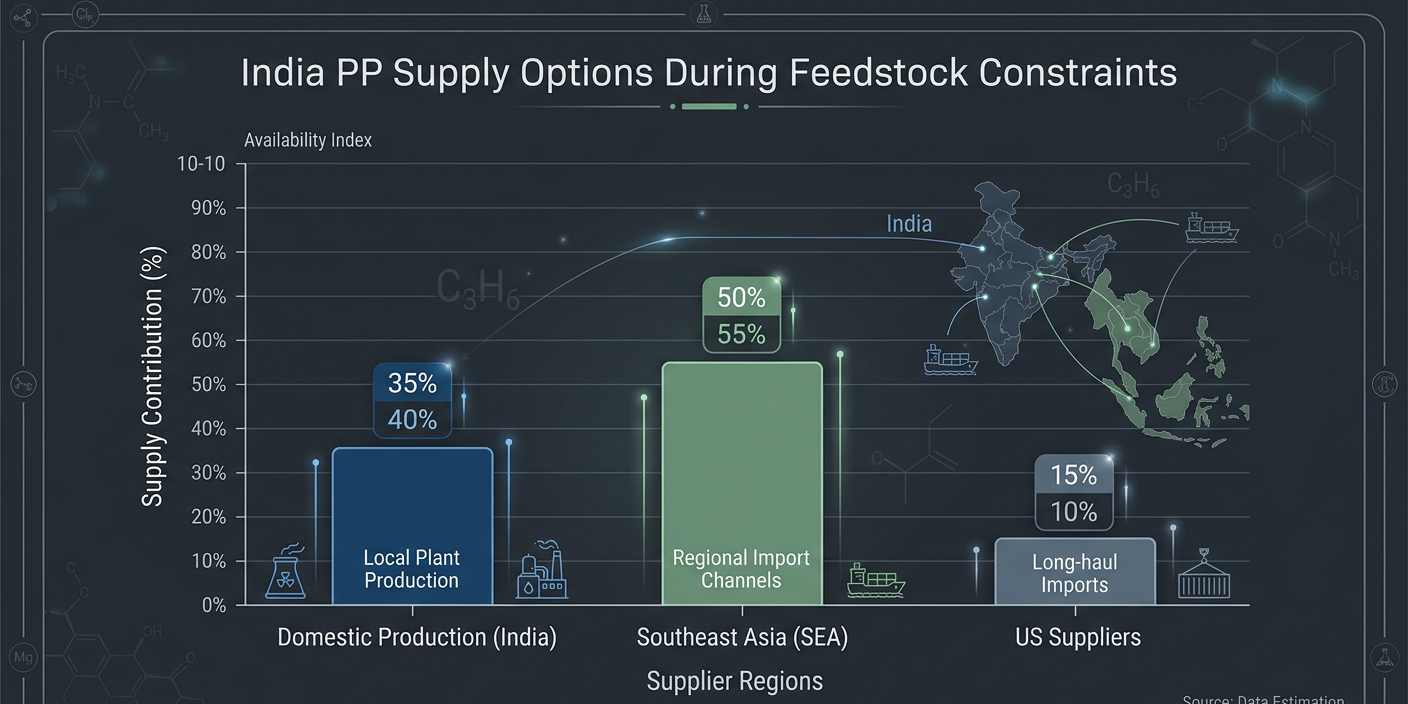

India’s polypropylene market is entering a challenging period as government feedstock restrictions affect around 80% of domestic PP capacity. The curbs have reduced feedstock availability for producers, creating tighter supply conditions for buyers across packaging, textiles, automotive and industrial sectors.

Domestic producers have already increased polypropylene prices by approximately Rs6/kg in June, with further adjustments expected if supply pressure continues. At the same time, Southeast Asian suppliers in Thailand and Vietnam have started attracting Indian buyers with competitive offers, creating a shift in import discussions.

For procurement teams, the current market requires faster supplier evaluation and stronger sourcing flexibility, especially before India’s temporary petrochemical duty waiver expires on June 30.

Polypropylene production depends heavily on reliable access to feedstocks such as naphtha and LPG. During periods of energy pressure, governments may redirect these resources toward fuel requirements, reducing availability for petrochemical production.

India’s current restrictions reflect this balancing effort between energy security and industrial demand.

The impact has been visible across the PP supply chain:

Producers face tighter access to raw materials needed for polymer production.

Operating flexibility decreases when feedstock allocation changes.

Domestic availability becomes more limited during periods of strong demand.

Buyers may need to look outside India for additional volumes.

Polypropylene is a critical material for many industries, making supply consistency a priority for manufacturers.

Indian polypropylene producers have responded to tighter feedstock conditions by increasing domestic prices. The market has already seen a Rs6/kg increase during June, with additional increases possible if supply remains constrained.

However, price movements are not only determined by domestic availability. International pricing and import competition also influence buyer decisions.

Current market conditions show a mixed picture:

Domestic supply is becoming tighter.

Imported material is becoming more attractive for some buyers.

Global PP prices remain influenced by energy costs and regional demand.

Importers must consider freight, duties and delivery timelines.

Argus assessed PP raffia prices in India at USD 1,250 to 1,310 per tonne CFR India on June 5, compared with USD 1,350 to 1,430 per tonne CFR India on April 10. This indicates that international price levels have softened even as domestic supply concerns increase.

Southeast Asian producers, particularly from Thailand and Vietnam, have become increasingly relevant for Indian PP buyers. Competitive offers from these regions are encouraging companies to explore alternative supply channels.

Import sourcing can provide benefits such as:

Additional supply security during domestic shortages.

More competitive price comparisons.

Reduced dependence on local production availability.

Greater negotiating power with suppliers.

However, buyers must also evaluate quality consistency, shipment timing and long-term reliability before switching suppliers.

The timing of the PP supply disruption creates additional pressure because India’s temporary petrochemical duty waiver is scheduled to expire on June 30. The waiver has supported imports by reducing landed costs for several critical chemical products.

For PP buyers, the expiry creates a key decision point:

Import before June 30 to benefit from current conditions.

Wait for potential market adjustments after the duty change.

Secure alternative suppliers before demand increases.

Review inventory levels based on production requirements.

The combination of domestic supply constraints and possible duty changes makes purchasing decisions more complex.

The polypropylene market will depend on several variables over the coming weeks. Buyers should track both domestic policy decisions and international supply trends.

Important factors include:

Feedstock availability: Restoration of naphtha and LPG access will influence producer operating rates.

Import economics: Duties, freight costs and currency movement will determine the attractiveness of overseas material.

Regional production: Supply conditions in Southeast Asia, the Middle East and the US will affect export availability.

Demand recovery: Packaging and industrial demand will shape purchasing activity.

Producer pricing strategies: Domestic manufacturers may adjust prices depending on supply pressure.

Procurement teams that monitor these factors can respond faster when market conditions change.

The current situation highlights the importance of supplier diversification. Companies that depend only on domestic PP sources may face greater exposure during supply disruptions.

Buyers should consider:

Qualifying suppliers from Southeast Asia.

Reviewing US export opportunities.

Building relationships with multiple producers.

Testing alternative grades where technically possible.

Maintaining flexible purchasing agreements.

Supplier qualification should happen before shortages become severe. The process requires technical approvals, documentation checks and logistics planning.

PP buyers in India are facing a narrow window to strengthen supply security. The combination of feedstock restrictions, domestic price increases and the approaching duty waiver deadline requires careful planning.

Recommended actions include:

Confirm upcoming production requirements.

Request updated import offers from qualified suppliers.

Compare domestic and overseas landed costs.

Review inventory coverage for the next several months.

Avoid relying on a single supply channel.

Companies that prepare early can reduce the risk of sudden cost increases or material shortages.

India’s polypropylene market is likely to remain sensitive until feedstock availability improves and supply chains regain stability. The current disruption shows how quickly energy policies can influence chemical production and downstream industries.

For buyers, the priority is maintaining supply continuity while managing costs. Import qualification, supplier diversification and active market monitoring will become increasingly important strategies in a volatile environment.

The companies that secure reliable sources before conditions tighten further will have stronger control over procurement decisions. Ready to source from verified global suppliers? Explore competitive offers on our platform today.

Featured Product

Found this useful?

Continue Reading

June 2026 is the most consequential month for India's chemical industry in years.

The Nylon 66 market has shifted from supply shortages to persistent oversupply in just a few years. New Chinese capacity, weak automotive demand and upcoming adiponitrile projects are reshaping global pricing power. Procurement teams now have a rare opportunity to secure favorable long-term contracts.

Hydrazine hydrate remains one of the chemical industry's most specialised and tightly regulated products. Growing pharmaceutical demand, industrial water treatment applications and evolving transport regulations are reshaping global procurement strategies in 2026.