The Path2Zero framework sets an ambitious timetable for industry to cut net emissions to zero by 2050. In the chemical sector, however, the deployment of carbon capture, utilization, and storage (CCUS) has remained far behind the projected curve, creating a widening “delay” that signals systemic obstacles. Understanding this lag is essential for designing interventions that can mobilize the capital, technology, and policy momentum needed to keep the sector on track.

Understanding Path2Zero and the Chemical Sector

What is Path2Zero?

Path2Zero is a decarbonization roadmap that maps out the technology, capital, and policy actions required for each industrial sector to reach net‑zero emissions. It identifies key milestones and the projected dates at which those milestones should be achieved to avoid catastrophic climate change.

Why the Chemical Industry Is a Key Player

The chemical industry is a major source of hard‑to‑abate CO₂, contributing roughly 8% of global industrial emissions. Its products—fertilizers, plastics, and specialty chemicals—are indispensable to modern life, making industrial decarbonization both a technical and a socio‑economic imperative.

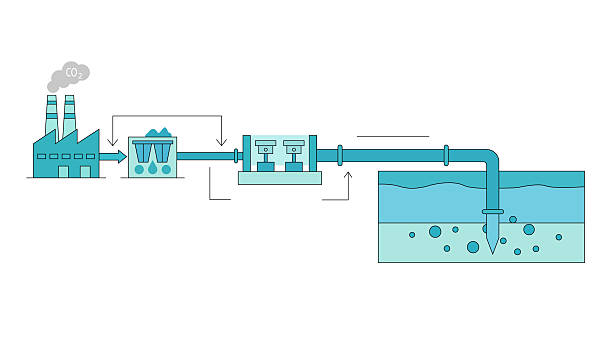

Current State of Carbon Capture Deployment

Commercial CCUS Projects: Numbers & Trends

As of 2025, only a handful of commercial CCUS facilities have reached full production in the chemical sector, with cumulative captured volumes under 5 Mt CO₂ yr⁻¹. In contrast, the Power sector has surpassed 200 Mt CO₂ yr⁻¹. The disparity underscores a lag in technology readiness and market confidence.

Barriers to Scale

Technological maturity: Capture units for high‑temperature, high‑pressure processes typical in chemicals are less mature compared to post‑combustion capture in power plants.

Capital intensity: Upfront CAPEX can exceed US$1.5 bn per 100 kt CO₂ yr⁻¹, a cost that many operators are unwilling to absorb without guarantees.

Uncertain economics: The price of CO₂ in existing markets is too low to justify capture without policy support.

Infrastructure gaps: Pipelines and storage sites are scarce, especially in regions with dense chemical clusters.

Regulatory uncertainty: Differing jurisdictional frameworks create hesitancy among investors.

Policy Mechanisms to Accelerate Investment

Carbon Contracts for Difference (CCDCs)

CCDCs offer a price floor for CO₂ emissions, guaranteeing a minimum revenue for captured CO₂. This mechanism reduces investment risk by decoupling profitability from volatile carbon markets. When paired with a target price that reflects the true social cost of carbon, CCDC can unlock billions in private capital.

Financial Instruments and Incentives

Tax credits and rebates: Proven‑technology credits can offset a significant portion of CAPEX.

Low‑interest green bonds: Issued by governments or public entities to finance CCUS infrastructure.

Public‑private partnerships (PPPs): Share risks and benefits between state actors and the private sector.

Carbon leakage safeguards: Policies that protect domestic industries from unfair competition.

Case Studies: Low‑Carbon Chemicals on the Rise

ಭಾರತದ Example: Ethylene Production with CO₂ Capture

One pilot in India has integrated a post‑combustion capture unit into an ethylene cracker, achieving a 20% reduction in net emissions. The project leveraged a CCDC that set a floor price of US$30 t⁻¹, making the economics viable for the plant operator.

European Example: Ammonia with Direct Air Capture

In Germany, a commercial-scale direct air capture (DAC) plant supplies CO₂ to an ammonia synthesis facility. The DAC unit, operating at 99% purity, allows the ammonia to be sold as a low‑carbon feedstock, opening a new market niche for “green ammonia.”

The Path2Zero delay in the chemical manufacturing sector is a clear signal that current policy and market mechanisms are insufficient to drive the rapid deployment of CCUS. By implementing robust carbon contracts for difference, aligning financial incentives, and fostering public‑private collaborations, governments can transform the economic calculus for chemical producers. The result will be a faster transition to low‑carbon chemicals, a healthier climate, and a more resilient industrial ecosystem.