Article

Jun 19, 2026schedule5 Min Read

Personal Care Ingredients: Cocamidopropyl Betaine, Glycerin.

The personal care ingredients market is navigating a dual challenge in 2026: elevated feedstock costs

Full Reportarrow_forward

prodchem

Jun 12, 2026

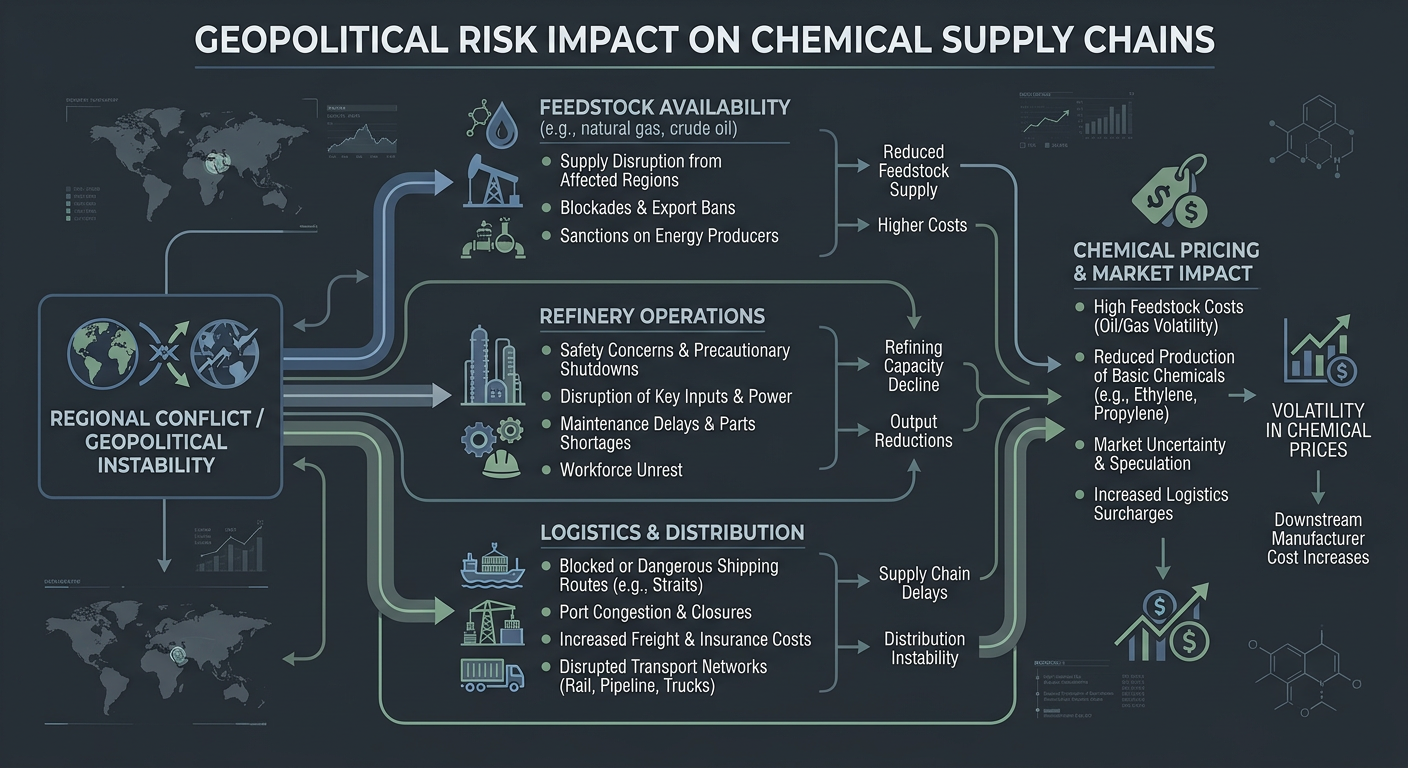

A missile strike targeting Israel’s Haifa region has placed a major petrochemical facility back under market attention, raising concerns about potential disruption to regional energy and chemical supply chains. The Haifa refinery and associated petrochemical complex represent a key industrial hub that connects crude processing, fuel production and chemical feedstock supply.

The facility has a refining capacity of approximately 197,000 barrels per day and supports Israel’s domestic chemical industry through integrated production systems. While damage has not been confirmed, the incident introduces another layer of uncertainty for chemical buyers already navigating geopolitical risks.

For procurement teams, the key issue is not only whether physical damage occurred, but how markets respond to the possibility of further escalation.

Integrated refinery and petrochemical facilities play an important role because they convert crude oil into fuels and chemical building blocks used by downstream industries. Any interruption can affect both local supply and regional trade flows.

The Haifa complex supports production chains connected to:

Refinery outputs used in energy markets.

Chemical feedstocks required for industrial manufacturing.

Domestic supply networks serving Israeli industries.

Regional trade relationships linked to Middle East energy flows.

A disruption at a major integrated facility can create uncertainty even before actual supply shortages develop. Buyers often react by reviewing inventories, alternative suppliers and future purchasing plans.

The immediate market impact depends on the extent of any damage and the time required for inspection or repairs. If operations continue normally, the effect may remain limited. If the facility experiences extended disruption, chemical buyers could face tighter regional supply conditions.

Potential consequences include:

Reduced availability of certain chemical feedstocks.

Higher demand for alternative supply sources.

Increased logistics pressure in nearby markets.

Greater uncertainty around regional pricing.

Chemical producers and distributors typically respond to supply risks by adjusting inventories and securing replacement volumes. This can influence market sentiment even without a confirmed production shutdown.

The Haifa strike comes at a sensitive time for energy markets. Crude oil prices recently declined as expectations improved around supply recovery and regional ceasefire developments.

However, renewed tensions could change market expectations quickly.

Energy-linked chemical markets respond strongly to geopolitical developments because:

Crude oil prices influence feedstock costs.

Refinery disruptions affect product availability.

Shipping risks can increase freight and insurance costs.

Buyers may increase inventories during uncertainty.

Market confidence can shift faster than physical supply conditions. Chemical buyers often need to monitor both actual production data and market sentiment.

The chemical industry operates through interconnected global supply networks. A regional disruption can affect companies far beyond the location of the event.

Key risks include:

Feedstock availability changes.

Delays in regional exports.

Higher transportation costs.

Increased demand for alternative suppliers.

Contract uncertainty.

Companies sourcing chemicals internationally should maintain visibility across suppliers, logistics providers and regional market conditions.

A strong sourcing strategy includes backup options before disruptions occur, rather than searching for replacements after supply problems begin.

The Middle East remains one of the most important regions for global chemical production and exports. Buyers worldwide depend on producers in the region for polymers, solvents, intermediates and other industrial chemicals.

A disruption affecting regional confidence could influence:

Export availability.

Buyer purchasing behaviour.

Spot market activity.

Regional price differences.

The actual impact will depend on whether the Haifa facility continues operations and whether wider geopolitical conditions remain stable.

Chemical buyers should avoid making decisions based only on short-term market reactions. Instead, procurement teams should evaluate supply exposure and prepare for multiple scenarios.

Recommended actions include:

Review supplier concentration and identify alternative sources.

Monitor refinery and petrochemical operating updates.

Assess inventory coverage for critical materials.

Maintain communication with suppliers about production status.

Evaluate contract flexibility during uncertain conditions.

Companies with diversified sourcing networks usually have more options when markets become unstable.

If regional supply risks increase, buyers may look toward alternative producers in Asia, Europe and North America. However, switching suppliers requires technical approvals, quality verification and logistics planning.

Alternative sourcing decisions should consider:

Product specifications.

Delivery timelines.

Regulatory requirements.

Long-term supplier reliability.

Quick market changes can create opportunities, but buyers need structured qualification processes to avoid supply disruptions later.

The Haifa petrochemical facility strike highlights how geopolitical events can quickly influence chemical markets. Even without confirmed damage, the situation demonstrates the importance of supply chain awareness.

Chemical buyers should continue monitoring refinery operations, regional developments and crude oil market reactions. Stability in the Middle East remains a major factor affecting global energy and chemical pricing.

The companies that maintain flexible sourcing strategies and strong supplier relationships will be better prepared for unexpected market changes. Ready to source from verified global suppliers? Explore competitive offers on our platform today.

Featured Product

Found this useful?

Continue Reading

The personal care ingredients market is navigating a dual challenge in 2026: elevated feedstock costs

Acrylonitrile markets entered Q2 2026 under significant pressure as feedstock volatility, high energy costs and tight supply pushed prices upward. Buyers across ABS plastics, acrylic fibers and carbon fiber precursors now face rising costs, longer lead times and increasingly complex procurement decisions.

Guinea’s bauxite export controls could reshape China’s aluminium supply chain, affecting alumina production, caustic soda demand and chemical procurement decisions. Buyers need to understand the downstream impact of changing raw material policies.