Introduction

The Asia‑Pacific region remains the world’s fastest growing market for specialty chemicals, with distributors playing a pivotal role in bridging global producers and local end‑users. In 2026, the competitive landscape is defined by strategic expansions, Hormuz‑independent sourcing, and a surge in regional specialists that bring localized expertise to complex supply chains.

Key Trends Shaping the Distribution Market

Digital Transformation – End‑to‑end visibility through blockchain and AI‑driven demand forecasting.

Geopolitical Shifts – Diversification away from Middle‑East crude to alternative feedstock sources.

Regulatory Tightening – Stricter safety and environmental standards driving higher quality controls.

SME Demand – Small and medium enterprises requiring flexible delivery and after‑sales support.

ICIS Rankings Context

ICIS, the leading market intelligence provider, now incorporates ESG scores and regional market share into its rankings. The 2026 list reflects not only revenue but also the ability to adapt to the changing regulatory and geopolitical climate.

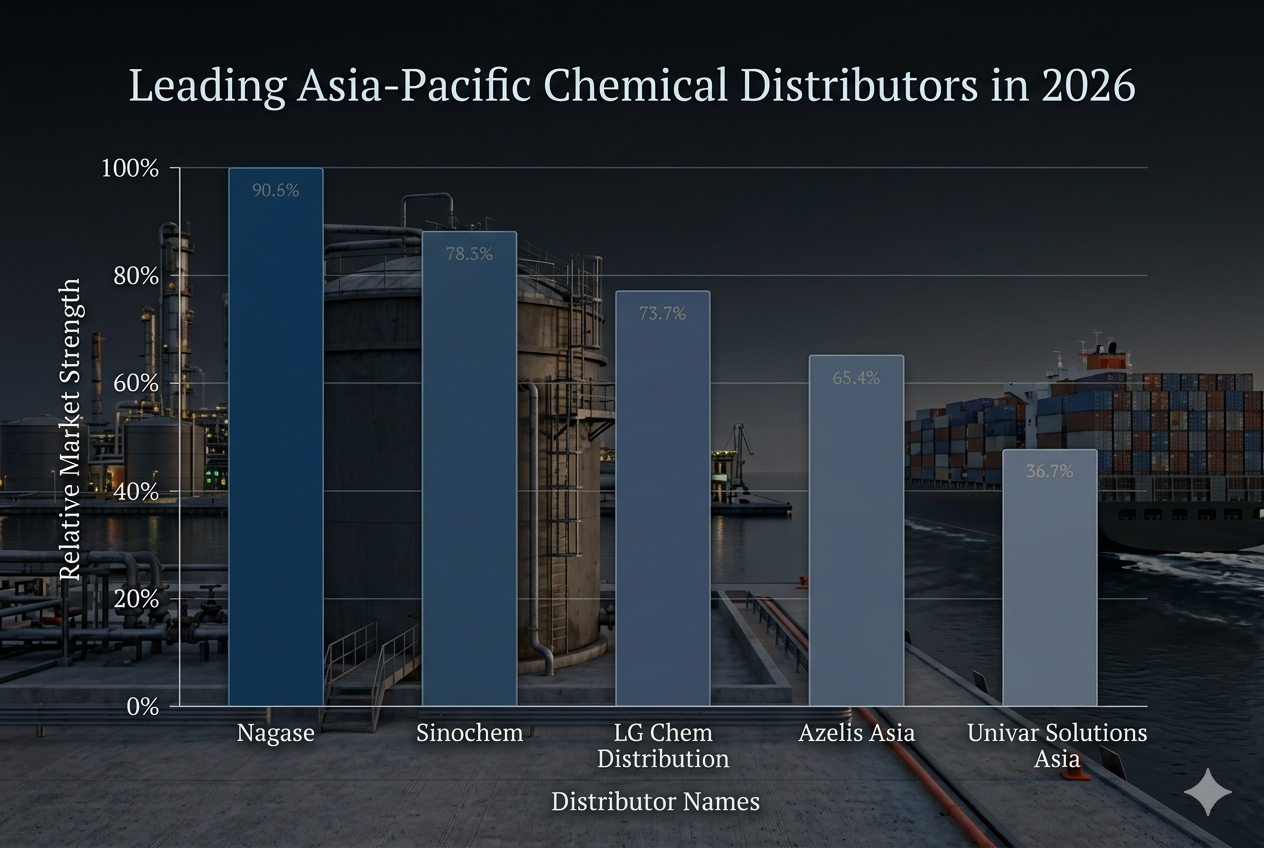

Top 10 Asia‑Pacific Chemical Distributors 2026

1. Nagase (Japan)

With a market share of 12% in the region, Nagase continues to dominate through its integrated logistics network and focus on high‑value specialty chemicals. Their investment in renewable feedstock sourcing has reduced dependency on Hormuz‑linked oil products.

Global reach: 45 countries

Core focus: Catalysts, fine chemicals, polymer additives

Digital platform: Real‑time inventory and traceability dashboard

2. Sinochem (China)

Sinochem’s expansion into Southeast Asia has positioned it as the second‑largest distributor. The company’s vertical integration—from petrochemical production to end‑user distribution—ensures low lead times and competitive pricing.

3. Lotte Chemical (South Korea)

Lotte Chemical leverages its robust supply chain and strong domestic customer base to offer a wide range of specialty chemicals, including adhesives and coatings.

4. Emory Chemicals (Australia)

Emory focuses on regional distribution of industrial gases and specialty additives, capitalizing on Australia’s stable political climate and proximity to New Zealand and the Pacific.

Regional footprint: 7 countries

Key products: Solvents, surfactants, and performance additives

5. China Chemical Industry Co. (China)

China Chemical’s aggressive strategy in the ASEAN market, through strategic partnerships and localized warehousing, has boosted its presence in the specialty chemicals arena.

Lead products: Acids, bases, and specialty intermediates

Expansion: 4 new warehouses in 2026

6. Jindal Chemicals (India)

Jindal’s focus on the Indian sub‑continent and its role as a key supplier for the pharmaceutical and agrochemical sectors have propelled its regional dominance.

7. Indorama Ventures (Thailand)

Indorama’s extensive petrochemical base supports its distribution network, with a strong emphasis on sustainability and circular economy initiatives.

8. Asian Chemical (Singapore)

Asian Chemical’s strategic location in Singapore allows it to act as a hub for chemical distribution across the Pacific Rim, offering rapid delivery and flexible logistics solutions.

Hub capacity: 500,000 cubic meters

Services: Cold chain, hazardous material handling

9. PetroChina (China)

While primarily a producer, PetroChina’s distribution arm has secured a significant share of the specialty chemicals market through direct sales to industrial manufacturers.

Direct sales: 30% of revenue

Key markets: Automotive, electronics, and construction

10. Wanhua Chemical Group (China)

Wanhua’s emphasis on polymer additives and high‑performance materials has positioned it as a top distributor for the automotive and construction sectors in the region.

Regional Specialists: The New Frontier

Beyond the global giants, a wave of regional specialists is redefining the distribution model. These companies focus on niche markets, local regulatory compliance, and personalized customer service.

PhilChem Solutions – Specializes in specialty additives for the food and beverage industry in the Philippines.

KorChem International – Focuses on eco‑friendly solvents for Korea’s growing green chemistry sector.

Vietnam Chemical Partners – Provides tailored solutions for the rapidly expanding textile and apparel industry.

Impact on Supply Chains

The combined effect of these distributors is a more resilient, diversified, and transparent supply chain. Digital platforms now enable real‑time tracking of shipments, while ESG commitments drive reduced carbon footprints across the network.

Conclusion

In 2026, the Asia‑Pacific chemical distribution scene is marked by a blend of established powerhouses and agile regional specialists. Nagase and Sinochem set the benchmark for scale and integration, while emerging players bring localized expertise and sustainability to the forefront. Together, they are reshaping the way specialty chemicals flow from global producers to regional end‑users, ensuring a more responsive and responsible chemical industry across the Asia‑Pacific.