Wood Mackenzie's "Condition Critical" Assessment: Three Months Later

terminal

prodchem

Jul 9, 2026

In rapidly changing industries, one of the most useful analytical exercises is to revisit earlier forecasts and compare them with subsequent developments.

Rather than asking whether a forecast was perfectly accurate, procurement professionals should evaluate whether the underlying analytical framework continues to explain market behaviour.

Three months after Wood Mackenzie characterised the petrochemical industry as being in a "Condition Critical" state, a substantial body of published industry information is now available for comparison.

The latest C&EN Global Top 50, together with publicly announced restructuring activity across the chemical sector, provides an opportunity to assess how the industry's direction has evolved.

The Industry Was Already Under Pressure

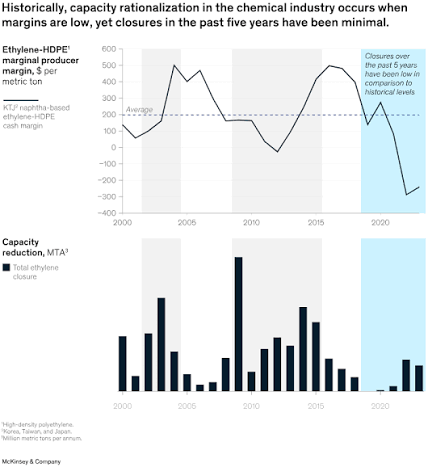

When Wood Mackenzie published its assessment, the petrochemical sector was already facing several structural challenges.

These included:

Global commodity overcapacity.

Weak downstream industrial demand.

Margin compression.

Reduced operating rates.

Slowing capital investment.

Increasing regional competition.

These conditions had developed before subsequent geopolitical events added further complexity to global supply chains.

Subsequent Industry Data Shows Continued Pressure

The latest published financial results continue to indicate that many commodity petrochemical producers operated in an exceptionally challenging environment.

Industry developments have included:

Revenue pressure among major integrated producers.

Continued earnings weakness in several commodity businesses.

Ongoing portfolio optimisation.

Capacity rationalisation in selected regions.

Greater capital discipline.

These trends are broadly consistent with an industry navigating the lower phase of the capital cycle.

Europe Continues Restructuring Commodity Capacity

One of the most visible developments during recent months has been continued restructuring within parts of the European commodity chemical industry.

Public announcements have highlighted:

Portfolio reviews.

Asset optimisation.

Capacity adjustments.

Corporate restructuring.

Increased focus on higher-value specialty businesses.

These developments suggest companies are responding to long-term competitive pressures rather than treating current market conditions as purely temporary.

Corporate Transactions Reflect Structural Change

Recent corporate transactions within the chemical sector also reinforce the broader restructuring trend.

Rather than expanding commodity production aggressively, many companies continue focusing on:

Portfolio simplification.

Operational efficiency.

Strategic acquisitions.

Divestitures of non-core assets.

Capital allocation discipline.

For procurement professionals, these developments illustrate that corporate strategy increasingly prioritises resilience and returns on capital over production growth alone.

The Capital Cycle Framework Remains Relevant

One reason the earlier analysis continues to resonate is that it aligns closely with the chemical industry's long-established capital cycle.

Typical characteristics near the lower phase of the cycle include:

Excess production capacity.

Reduced profitability.

Lower investment.

Asset rationalisation.

Consolidation activity.

These characteristics remain evident across many commodity petrochemical markets today.

Procurement Should Distinguish Between Cyclical and Structural Change

One of the most valuable lessons from the past several months is that not every market disruption produces permanent structural change.

Procurement professionals should separate developments into two categories.

Cyclical developments include:

Temporary demand weakness.

Inventory corrections.

Commodity price volatility.

Short-term logistics disruption.

Structural developments include:

Permanent capacity closures.

Long-term portfolio restructuring.

Regional shifts in manufacturing competitiveness.

Changes in investment priorities.

Business model transformation.

This distinction helps procurement teams determine which changes require tactical responses and which warrant long-term sourcing strategy adjustments.

What This Means for Procurement Strategy

The alignment between multiple published industry assessments reinforces several procurement priorities.

Differentiate commodity suppliers from specialty chemical businesses.

Evaluate supplier investment and restructuring announcements.

Diversify sourcing for strategically important raw materials.

Build flexibility into long-term supply agreements.

Review supplier exposure to regional competitive pressures.

Rather than reacting to individual headlines, procurement decisions should be based on consistent patterns emerging across multiple independent sources.

An important benefit of reviewing earlier industry analysis is identifying which analytical frameworks remain useful.

When independent publications reach similar conclusions using different methodologies, procurement professionals can have greater confidence that they are observing broader structural trends rather than isolated company events.

However, validation should not be interpreted as proof that every earlier prediction has been fulfilled. Market forecasts remain subject to uncertainty, and geopolitical events, policy changes and macroeconomic conditions can still alter future outcomes.

For this reason, procurement teams should use published outlooks as decision-support tools—not as fixed forecasts.

Looking Ahead to H2 2026

Three months after Wood Mackenzie's "Condition Critical" assessment, subsequent industry developments broadly continue to support its central observation that the petrochemical sector has been operating through an exceptionally challenging phase of the capital cycle. The latest C&EN Global Top 50, continued portfolio restructuring, capacity rationalisation and disciplined capital allocation all point toward an industry adapting to sustained competitive pressure rather than expecting a rapid return to previous market conditions.

For procurement professionals, the value of this comparison lies less in determining whether every individual forecast proved correct and more in understanding that several independent sources now describe similar structural themes. Commodity petrochemical markets remain under pressure, specialty businesses continue demonstrating greater resilience and companies are increasingly reshaping portfolios to improve long-term competitiveness. These recurring signals provide a stronger basis for strategic planning than any single report viewed in isolation.

The key lesson for H2 2026 is that procurement strategy should be informed by multiple validated sources rather than relying on one market outlook. Combining industry reports, company financial disclosures, restructuring announcements and supplier engagement provides a more balanced assessment of future supply conditions. Organisations that continuously compare forecasts with actual market developments will strengthen procurement decision-making, improve supplier risk management and build more resilient sourcing strategies for the years ahead.

Ready to source industrial and specialty chemicals from verified global suppliers? Explore competitive offers on our platform today.